A Cost of Production Report (CPR) serves as a comprehensive document that outlines the total cost incurred during the production process. By dissecting the nuances of these costs, manufacturers can identify inefficiencies, adjust pricing strategies, and enhance their decision-making process. The cost of production report (CPR) is a document used in process costing system that summarizes information about the flow of units and costs through the work in process account of a processing department.

What are the main reasons of using a job-order costing system?

- Gathering cost data is not a one-time activity, but a continuous process that requires regular monitoring and updating.

- Auditors examine the methods used to allocate overhead to ensure they are reasonable and consistently applied.

- It involves examining financial information related to expenses incurred during a specific period.

- This data encompasses a wide array of variables, from direct costs like raw materials and labor to indirect expenses such as overhead and maintenance.

From the perspective of a floor manager, the CPR is a tool for day-to-day operational control, ensuring that resources are being used efficiently. For an accountant, it’s a ledger that must balance, reflecting the intricate relationship between costs and output. Meanwhile, a strategic planner views the CPR as a map, guiding long-term investments and the scaling of production capacities. Measures the amount of work done during a period, expressed in fully completed units. Accruing tax liabilities in accounting involves recognizing and recording taxes that a company owes but has not yet paid. This is important for accurate financial reporting and compliance with…

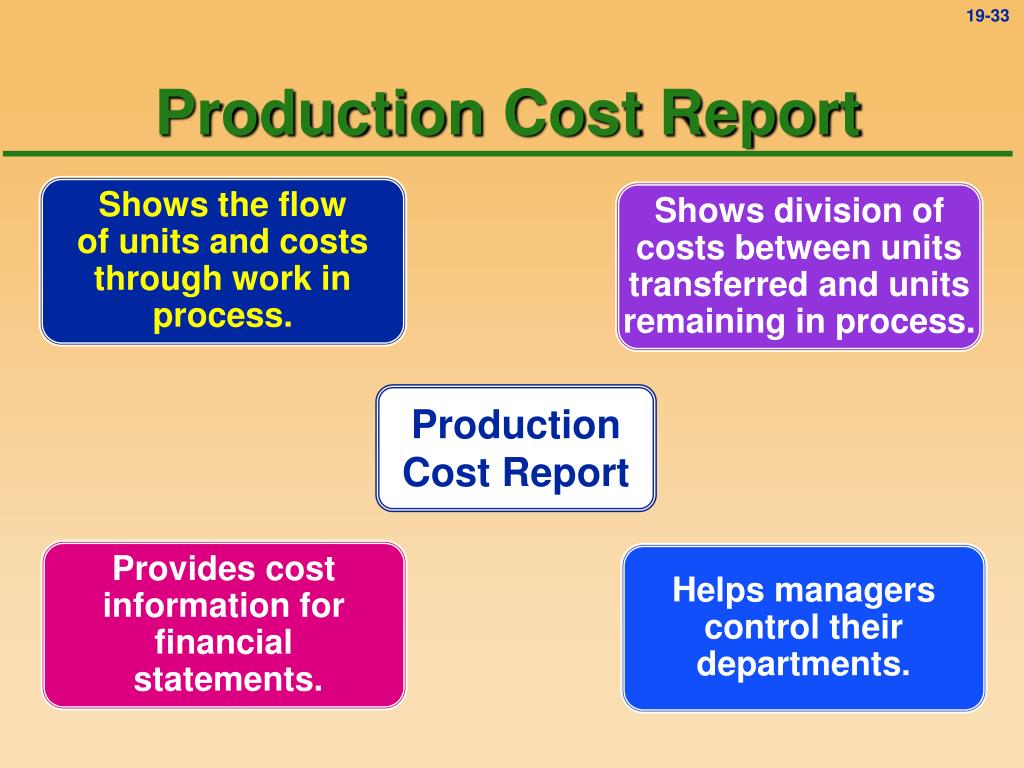

Production cost report

A cost of production report is a detailed document that summarizes the costs incurred during a specific accounting period in a process costing system. It provides insights into the production process by outlining direct materials, direct labor, and manufacturing overhead costs, allowing businesses to analyze their efficiency and cost-effectiveness. This report is essential for tracking production costs and valuing inventory in industries where products are produced in a continuous flow. It’s a vital management document that provides important information to managers in numerous areas.

Strategic Decision-Making with Cost of Production Data

Understanding the role of the cost of production in manufacturing is pivotal for any business aiming to maintain a competitive edge in the market. The cost of production encompasses all expenses incurred to bring a product to market, including raw materials, labor, and overhead. It directly influences pricing strategies, profit margins, and decision-making processes. By meticulously analyzing production costs, manufacturers can identify inefficiencies, optimize resource allocation, and enhance product value.

Google Pixel 9 Pro reportedly costs 11 per cent less to manufacture as compared to last year’s Pixel 8 Pro.

And some of the relevant cost subcategories may be excavation, concrete, steel, wood, tiles, pipes, wires, etc. This information is summarized nicely in a standard format with the production cost report. Conversion costs refer to the direct labor and manufacturing overhead vintage tobacco expenses incurred in the production process to convert raw materials into finished goods. In process costing, Cost of Production Report is also referred to as Process Cost Sheet. Cost of Production Report is prepared at the end of costing period, usually a month.

Cost categories are the broad groups of costs that are related to a common objective or function, such as labor, materials, equipment, travel, overhead, etc. Cost subcategories are the more specific types of costs that fall under each cost category, such as salaries, wages, benefits, supplies, consumables, rentals, fuel, etc. It is important to identify the relevant cost categories and subcategories that are applicable to the project, program, or activity being reported. This will help to organize and classify the cost data in a consistent and logical manner. For example, if the cost report is for a construction project, then some of the relevant cost categories may be site preparation, foundation, framing, roofing, plumbing, electrical, etc.

The accurate calculation of these costs not only reflects the efficiency of production processes but also impacts the pricing strategy, profitability, and competitive positioning of a company’s products. From the perspective of a cost accountant, the precision in these calculations ensures the integrity of financial reporting. Meanwhile, production managers view these costs as a measure of operational efficiency, and strategic planners use them to forecast and budget for future production cycles. Understanding the key components of a Cost of Production Report is crucial for any manufacturing business aiming to streamline its operations and maximize profitability. This report serves as a financial mirror, reflecting the detailed expenses incurred in the production process. By dissecting this report, stakeholders can pinpoint areas of cost savings, evaluate the performance of production methods, and make informed decisions about pricing strategies.

Cost of production report shows all the costs related to a particular department. It is not solely the outlined journal entries at the end of the month, instead additionally it is important for the presentation of costs accumulated throughout the month. The three basic cost behavior patterns are known as variable, fixed, and mixed. To predict what will happen to profit in the future, we must understand how costs behave with changes in the number of units sold (sales volume). Once the cost per unit is identified, the company assign this cost to the finished goods units and the work in process units.

By analyzing WIP Inventory, manufacturers can gain a clearer picture of their cost of production, identify areas for improvement, and better manage their resources. A Total costs to be accounted for (step 2) must equal total costs accounted for (step 4). Other names used for cost of production report are production cost report and production report. Process costing is preferred by companies that produce identical or similar products.